Diary of an investor: 03 - Wise plc

Valuation Date: 2 July 2024

Finding great companies takes time, but finding great companies at great prices can take an eternity. Yet, when you do encounter such opportunities, your serotonin and dopamine levels reach new highs. At least that’s what I felt while I was valuing Wise.

Overview

Wise (formerly TransferWise) is a London-based fintech company founded in 2011 by Taavet Hinrikus and current CEO Kristo Käärmann. The company had 12.8 million active customers in 2024, up from 6 million in 2021.

I've been personally using Wise's services since last year when I spent a semester abroad in Japan. My experience in handling international money transfers and daily payments has been overwhelmingly positive compared to traditional banks. Therefore, I was delighted to analyse a business for which I am a satisfied customer, which is quite uncommon.

A little bit about the company’s origin story: the two co-founders used to work in London and received their salaries in local currency. However, as they both had expenses in their homeland, they had to transfer money back to Estonia and pay the several hidden fees charged by banks for international payments, until they became fed up and founded Wise: a fintech company providing transparent and cheap

cross-border transfer services in 160 countries and 40 currencies for both individuals and businesses across the world.

Wise’s core value is transparency: the company’s mission is literally to bring transfer fees to 0 while exposing traditional banks’ obscure practices, often through provocatory marketing campaigns such as the one shown below.

As mentioned, Wise has a vast geographical reach, diversifying its revenue sources as follows: 32% from Europe, 21% from North America, 20% from the UK, 19% from Asia Pacific, and 8% from the rest of the world. All segments are growing fast at double-digit rates and, as the company obtains more licenses globally, further integration is expected.

One of the aspects that really struck me about Wise was its culture:

First, the reporting practices adopted by the company are among the best I’ve ever encountered: the management communicates business performance and outlook through clear and fair metrics, avoiding what Charlie Munger famously called “bullsh*t earnings” (YT video), therefore providing a sound starting point for the forecasting exercise. I am happy to admit that this is one of the few times where I considered the management’s mid to long-term guidance in my projections.

Second, earnings calls highlight the extraordinary attention put on the customer. Every remark, guidance, and comment is crafted with the customer’s needs in mind, aiming to enhance the user experience through lower prices, increased efficiency, or other initiatives. This mindset is being unfortunately replaced by profit maximisation approaches, often forgetting that in the long run, returns are obtained only if the customer is satisfied.

Finally, incentives between the management and shareholders are aligned, to say the least. The company undertook a direct listing of Class A shares (holding 1 vote each) in 2021, retaining control of non-transferable Class B shares (holding 9 votes per share and expiring in 2026) to guarantee the management’s control over the company’s mission. According to Factset, the CEO alone owns 18% of outstanding shares and 50% minus 1 share of voting rights. The direct listing further underlines the competence of the management, abstaining from raising unnecessary funds to avoid dilution of ownership.

Business Model

Before I break down Wise’s business model, I would like to briefly explain how traditional international money transfers work.

When we send money internationally, most of the transactions occur under what’s called correspondence banking: if your bank doesn’t have a direct relationship with the recipient’s bank (which is often the case), an intermediary bank will intervene to facilitate the transfer. Usually, the money is transferred to more than one intermediary, especially if the sender’s and recipient’s banks are regional. For every step, each party involved retains part of the transfer as a fee. Additionally, due to timezone differences and various country regulations, transfers might take a long time to complete. These are the reasons why we rarely know the precise amount of money that will reach the recipient and the exact time of its arrival.

In summary, traditional international transfers suck.

Now, on to Wise’s revolutionary business model.

Instead of relying on correspondence banking, Wise invented a peer-to-peer system that significantly increases efficiency and decreases costs. The company acts as a big matching service for your transfers. Let me illustrate with an example:

Assume A lives in Europe and wants to send money to B in the United States. Instead of transferring money overseas, Wise will collect the amount from A and store it in one of the company’s accounts held at a leading bank, in this case in Europe.

Parallely, C who lives in the U.S. wants to send money to D, living in Europe. At this point, Wise will simply send A’s money to D, and C’s to D, matching the transfers.

Here’s a YT video explaining it: Business Disruptors YT.

I know this sounds superficial, but expand this simple concept to a global network of partner banks and millions of daily transactions, and you have an incredible business. Additionally, Wise uses machine learning and AI to estimate liquidity requirements more efficiently, further optimising the system. Now we also understand why this is a business exhibiting strong economies of scale and network externalities: as more people join the platform, money can circulate more efficiently, bringing down costs and benefiting everyone.

For reference, a traditional international payment costs on average 6% of the amount transferred (source), while Wise charged only 0,67% in FY2024, almost 10 times cheaper.

Oh, and I didn’t mention that in the whole correspondence banking process, institutions always charge a hidden fee: a 1%-2% markup on the currency exchange rate. On the other hand, Wise uses the mid-market exchange rate, which is the midpoint between the buy and sell prices of two currencies in the global market, representing the fairest and most accurate exchange rate available. You can check for yourself how the company compares with other businesses on the rate and fees charged directly on Wise’s website: Wise Compare.

Finally, mind that Wise is NOT a bank, and doesn’t directly hold your money. Instead, it distributes part of the deposits to major banks (list) and invests the remaining amount in low-duration assets (usually government-issued securities), earning interest.

Products

Wise offers three main products: Wise Personal, Wise Business, and Wise Platform.

Wise Personal is designed for people living, working, and travelling abroad. Customers can open a Wise Personal account for free and use services including international transfers and currency exchanges in less than 2 days. Additionally, customers can order a physical debit card for a one-time payment of £7 (varies by country), or a free digital card.

Wise Business is instead the account designed for businesses (who would have said right?). It acts as an extended version of Wise Personal, allowing owners to make international payments and organise their finances efficiently, harnessing Wise’s open API.

Finally, Wise offers its infrastructure to partners through Wise Platform: banks, large businesses, and major enterprises can leverage the company’s network and technology to integrate Wise’s system into their offerings. Among the partners, we find NuBank, Interactive Brokers, Monzo, N26, Google Pay, Bank Mandiri, and Shinhan Bank.

Wise Personal accounts for 77.5% of underlying revenues (more on this later), and Wise Business accounts for the remaining 22.5% (note that Wise Platform revenues are split between Personal and Business accounts based on the partner’s end customer).

Unit Economics

Let’s delve more in-depth into Wise’s operations.

Unlike most financial institutions, Wise’s website offers a comprehensive and transparent list of all the fees charged for the company’s services: fees.

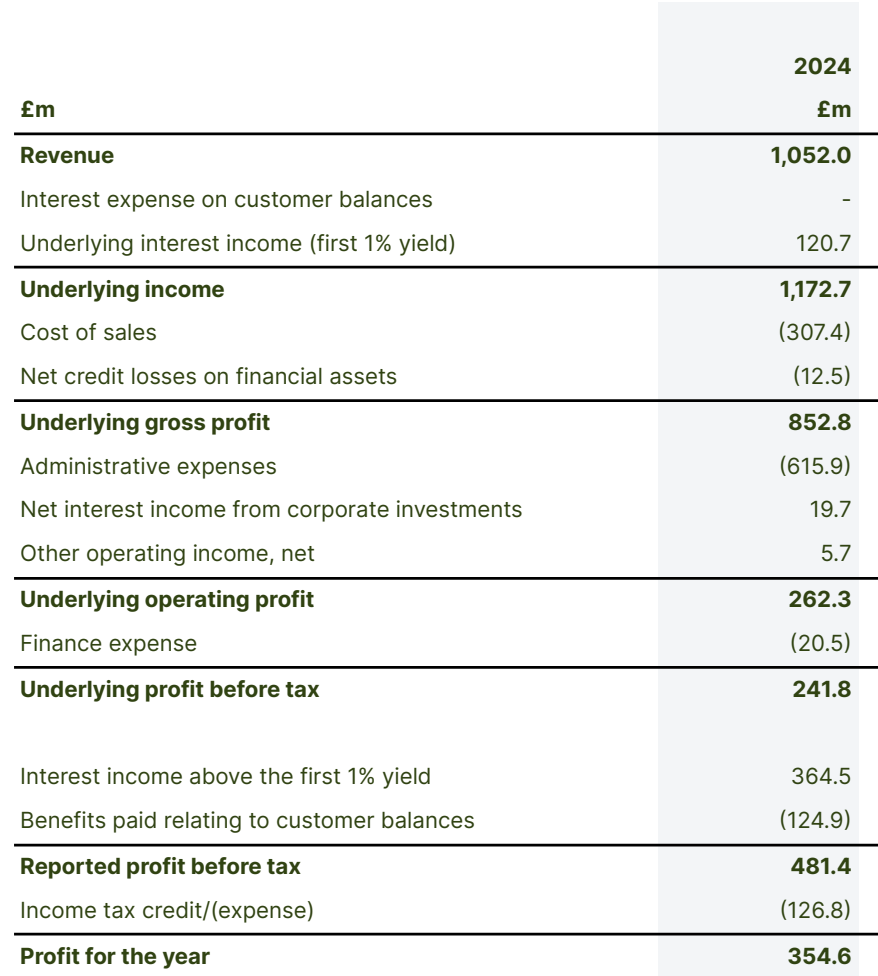

Wise doesn’t charge any subscription fees. Instead, revenues are derived from two main sources: transaction commissions and interest income. In FY2024 Wise recorded £1412m revenues.

For certain transactions (depending on the currency and the countries involved) the company charges a variable rate (0.67% in FY2024) on the amount sent. Additionally, Wise allows 2 free withdrawals for up to £200 a month. For every additional withdrawal, a fixed fee of £0.5+1.75% is applied. Finally, customers can invest in short-term securities to earn interest on deposits directly through Wise’s platform. For such a service, the company charges a 0.6% annual fee, which comprehends a 0.15% fee for the fund manager.

Fee-related revenues totalled £1052m in 2024.Because of high rates set by central banks worldwide to tame inflation, Wise has been earning unusually high interest on deposits and short-term investments. This source of income increased rapidly, going from representing just under 1% of total revenues in 2022 to 32% in the last year.

Interest income revenues amounted to £485.2m in 2024.

Wise’s management is aware that the revenues earned through interest income are only partially strictly operating. Therefore, to highlight the strength of the core operations the company reports its financials and provides guidance through what’s called “underlying income” (£1172.7), which considers only fee-related revenues and interest income derived from the first 1% of the gross yield (if interest rates are at 4%, underlying income considers revenues earned as if rates were at 1%). Therefore, of the £485.2m in interest income revenues, only £120.7m is considered underlying income. The remaining amount (£364.5m) is then added to the “underlying profit before tax”, providing the complete picture of the company’s operations.

Wise divides its core and non-core operations in reported financials to emphasise the robustness of its core business, which could’ve been under-appreciated if merged with non-operating activities. For reference, underlying income almost tripled from FY2021 (£421m).

Source: Wise annual report FY2024

Operating costs are mostly composed of COGS and SG&A expenses.

Cost of Sales comprises the costs directly related to the company’s operations: because Wise is not a bank, the company incurs small fees to process transfers and exchange currencies. Additionally, Wise can experience costs due to chargebacks and differences between the rate offered to customers and the one actually paid by the company (the mid-market rate offered to customers is locked for the entire duration of the transfer. Therefore, for particularly long/volatile transactions the company could bear unexpected costs)

Administrative costs include employee compensation, marketing, technology, consultancy, D&A, and others. It is interesting to note that employee compensation includes share-based compensation (SBC). The company does NOT adjust operating income for such measure, as is often and unfortunately the case with many tech companies. I’ll leave a link to Damodaran’s article on why SBC should be treated as a real expense: SBC Damodaran.

As mentioned before, Wise earns interest on the money deposited by its clients. However, the management feels that this isn’t entirely “fair” and gives back to customers part of the income received. Nevertheless, since Wise is not a bank and cannot distribute interest directly, the company employs other methods to compensate its users, primarily through cashback programs. For a complete description of the cashback rates applied by the company check this website. Similarly to interest earned above the 1% threshold, benefits paid to customers are then subtracted from the underlying profit before tax to reconcile the financial statements.

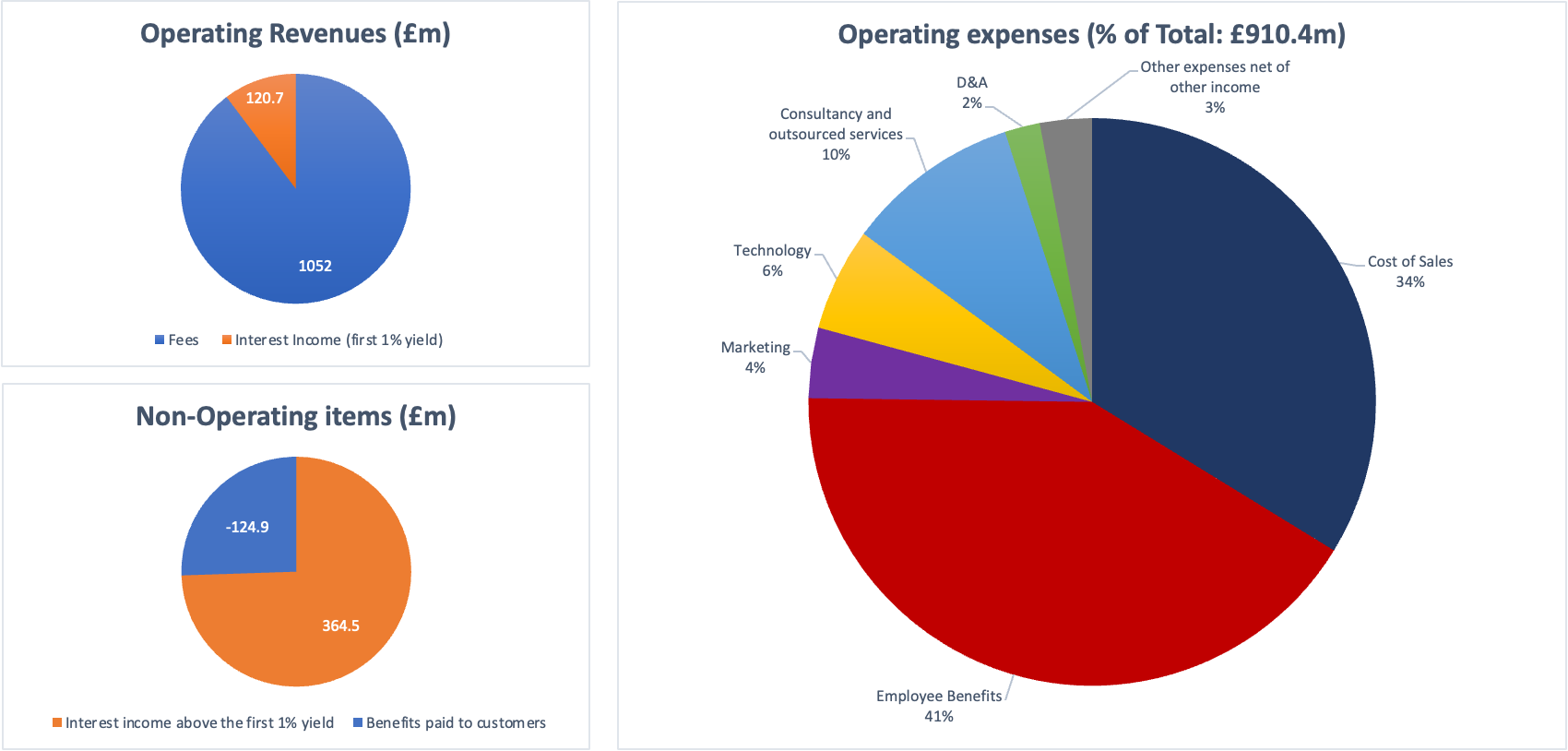

Here’s a visual breakdown of Wise’s unit economics for FY2024:

(Other expenses net of other income include: bad debt, capitalisation of staff costs, other administrative expenses, and income from corporate investments)

One of Wise’s strengths lies in its profitability: the company recorded an underlying EBIT margin of 22.37% and an underlying EBT margin of 20.6%, an incredible expansion from the EBT 10.7% level recorded in FY2021. If we consider non-operating items, the EBT margin soars to an outstanding 34%.

Finally, I want to spend a couple of words about CAPEX. The company’s business model is incredibly investment-light. Once the initial infrastructure is built, most of the spending is focused towards incremental projects, increasing efficiency and overall user experience. Interestingly enough, marketing, a key factor of success in the industry, accounts for only a small part of investments. This is possible because Wise’s strongest advertising tool is the word-of-mouth effect, which requires almost 0 CAPEX. Indeed, Wise estimates that 2/3 of customers join through a recommendation, and I’ve personally suggested the service to several friends.

Investments (calculated as Net CAPEX ± ΔNWC + Capitalised Investments) averaged only 4% of revenues in the past 3 years.

Competitive advantage

“Competitive advantage” became a concept so overused that it almost lost its meaning in the investing world. Therefore, I’ll try to be as clear as possible about what actually constitutes a moat for Wise. Competitive advantage is created when a company does something difficult to replicate by competitors and uncomfortable to adopt by incumbents. It is not derived from financial statements or ratios; instead, it is the foundation for the quality of these measures.

I’ll first start by analysing Wise’s position relative to incumbents.

In this case, incumbents are traditional banks, which handle most of the international transfer flow. Wise exhibits strong counter positioning, meaning that banks don’t want or can’t easily copy the company’s value proposition as it would hinder their existing strategy and be extremely expensive. There are several reasons for this:

Banks want to hold deposits, not transfer them: any bank’s business is based on holding deposits to give out loans, profiting from the spread between the interest paid and the interest charged. More deposits lead to more loans, which lead to more money. Wise’s business model connects several banks globally, and if any traditional bank were to build something similar, it would only facilitate deposit transfers. Therefore, traditional banks are hesitant to offer this service, facing a classic case of the innovator’s dilemma. Additionally, banks would need to renounce the revenues coming from high transfer fees and markups on exchange rates, further complicating the incumbent’s position. Eventually, banks will realise that this reform is inevitable as more customers join neo-banks and institutions offering Wise-like services because, in the long term, customer satisfaction wins.

The technology infrastructure would take years to complete: people often underestimate the complexity of building a solid technological infrastructure, thinking, “Just spend a lot of money and you’ll have the tech ready by next year.” However, developing an efficient system in a highly regulated industry is extremely difficult and time-consuming, particularly if you start from outdated technology such as the one used by traditional banks. Don’t forget that Wise was founded in 2011, 13 years ago. During the June 2024 earnings call, Wise’s CTO Harsh Sinha emphasised that CTOs at banks and enterprises understand that "it will require not months, but years to upgrade the systems." Instead, banks have now the option to switch their correspondent to Wise and utilise the company’s API, a solution enabled by Wise's recent integration into the Swift network.

Regulators continue to foster innovation: To worsen the incumbent’s position, regulations are becoming increasingly stringent in reducing transfer costs, which disproportionately affect lower-income families and migrants. Indeed, among the Sustainable Development Goals (SDGs) adopted by the United Nations, SDG 10 aims at reducing the average cost of remittances to 3% globally (link).

Banks are culturally “slow” and risk-averse: traditional banks are particularly subject to inertia. They’ve been doing the same business for decades and established relationships with partners that no longer sit at the innovation edge. Their business, key to society’s functioning, inherently imposes risk aversion and reluctance to change, as even minor adjustments ripple through the entire operations. As a result, banks often experience organisational inertia and lag behind in adopting revolutionary trends, while neo-banks and fintech companies thrive and expand rapidly.

For such reasons, it is in the banks’ best interest to collaborate with Wise-like platforms (or acquire them), rather than build this service in-house. We’ve already seen new fintech banks such as Monzo and NuBank, which have a different culture and are more responsive to change, starting to collaborate with Wise, and I believe that we will also see traditional banks pivot to such services.

I’ll now examine Wise’s competitive position against companies that currently offer a similar value proposition. Among these, we find Revolut, PayPal (Xoom), Remitly, MoneyGram, Western Union and several other smaller companies.

The industry is fragmented and a dominant design has not yet emerged, with all competitors showing different unit economics. Therefore, instead of describing each rival’s business model, I will highlight the areas where Wise performs better.

Price and speed: probably the most important factors of success in this industry, price and speed are key components to Wise’s competitive advantage. Most of the time, Wise is able to offer the best rates thanks to its scale, technology, and more importantly its cost structure: the company’s unique business model removes intermediaries and cuts costs, allowing for greater flexibility in pricing. Furthermore, thanks to its global network, Wise provides competitive prices also for less common currencies. In the few cases where competitors charge cheaper prices, Wise compensates through speed. In Q4 FY2024, 62% of transactions were executed immediately, 83% in <1 hour, and 95% in less than a day. Again, this is possible because of the company’s technology and global network.

Transparency: Wise is the only one consistently offering the mid-market exchange rate among existing competitors. In contrast, many rivals use proprietary rates that include a small markup. Moreover, Wise regularly publishes comparisons of its rates against those of competitors, keeping consumers well-informed about the industry. If you need information about a company in the sector, Wise likely has an article on it. I did find these analyses relatively unbiased, which makes sense since the company has nothing to hide—Wise’s services are the most competitive, and increasing available information will only strengthen its position.

Reputation: Throughout the years, Wise has established a strong reputation with its customers. The company’s efficiency, transparency, simplicity, and culture have all contributed to building Wise’s positive image. Different sources report Wise's Net Promoter Score (NPS) — a measure of customer satisfaction scoring companies from -100 to +100 (learn more) — ranging between 28 and 83, consistently higher than its competitors. For instance, Xoom has an NPS of -83, Western Union is at -15, and Revolut scores 8. Here’s a website where you can compare the NPS yourself: Comparably. Additionally, two-thirds of new customers come from referrals, further evidencing high customer satisfaction. Finally, Wise’s affiliates, such as NuBank, N26, Interactive Brokers, and Bank Mandiri, also have strong reputations, underscoring Wise's credibility as a business partner.

Compatibility: Wise’s platform is incredibly versatile and easy to adopt. Recently, the company joined the Swift network, making it easier for other banks to leverage Wise’s infrastructure. Additionally, since Wise is not a bank, both traditional and neo-banks are more likely to collaborate with Wise instead of competitors like Revolut, as there are fewer conflicts of interest and less direct competition. Therefore, Wise is in a sweet spot, offering high-quality services with the least risks.

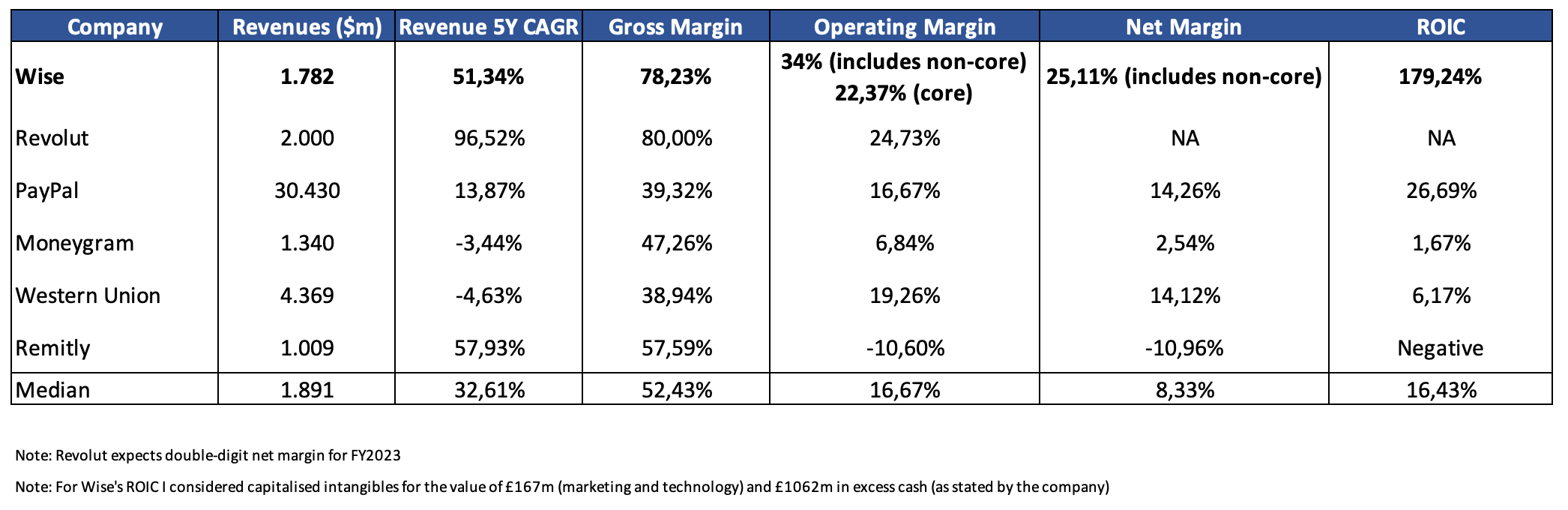

As mentioned, these factors are then reflected in financial metrics, and Wise shows best-in-class margins, ROIC, and growth when compared to competitors.

Here’s a brief summary:

Finally, a few thoughts about potential entrants: even if the industry is relatively investment-light, entering the market poses several challenges.

First and foremost, scale and first-mover advantages matter. To maintain its moat in a very competitive environment, Wise uses the following strategy: instead of letting margins expand as a result of economies of scale, the company artificially reduces its fees, therefore fixing revenue growth and margins to target values. This could sound strange as normally you want revenues and margins to grow as far as they can. But by embracing this tactic, Wise widens the gap between its prices and the ones offered by competitors (and potential new entrants), becoming increasingly appealing to new customers and partners. Therefore, the bigger the company gets, the more difficult it is for new entrants to match Wise’s offerings.

Second, the industry is heavily regulated, and obtaining the required licenses takes time. More specifically, Wise and its competitors need to obtain certifications from all the countries in which they operate. As a result, potential entrants must consider not only the length of the process but also the complexity of navigating different jurisdictions.

Finally, Wise and its competitors have a strong reputation and extensive networks. Existing relationships hinder the new entrants’ ability to form their own connections, and network externalities raise the aggregate value of Wise’s products, posing additional hurdles for new competitors.

Threats

Of course, the future is uncertain, and potential threats are always to be considered. Here’s a couple of things to keep an eye on:

Visa Direct and Mastercard Send: the two global giants rolled out their in-house platforms to facilitate international transfers. I didn’t discuss the two companies in the competitors segment because I believe that Wise, Visa, and Mastercard can co-exist and are complementary assets, rather than alternative ones. Indeed, Wise has been leveraging Visa Direct to achieve faster transfers since 2021 (link). Visa and Mastercard are often integrated into other service providers and focus primarily on card transfers, while Wise and similar platforms offer a greater range of services and target a slightly different customer segment (individuals, SMEs, and Neo-banks). Therefore, I am confident there is enough differentiation between Wise and Visa/Mastercard to guarantee a healthy coexistence.

Competition with current rivals: even though I believe Wise has the best competitive position over competitors, the industry is fragmented and is likely to stay that way. Intense competition contributes to downward price pressures, forcing Wise to keep lowering fees periodically to maintain its edge.

CBDCs: as many central banks experiment with digital currencies worldwide, some envision a future where FIAT currencies are useless. To me, this occurrence sounds improbable for two reasons:

First, an immense collaboration effort would be required to form a unified strategy among countries, an especially complex task as deglobalisation trends persist. Second, current payment infrastructures, including the Wise network, are far more efficient in terms of speed, price, and security when compared to blockchain or other systems.

Still, you might have a different view and should consider the matter for yourself.Achievement of Target Zero: if Wise were to achieve its Target Zero mission (providing international transfers for free), the company would need to monetise its services in other ways, which are not easily identifiable. I do believe that the management honestly wants to offer lower prices to customers, but I also think that “Target Zero” is part of Wise’s marketing strategy to establish itself as a customer-friendly company. Moreover, the pace at which Wise can reduce prices is relatively slow. Even if we assume the company will double its rate of price cuts compared to the past five years, free transfers wouldn't be achievable for at least 35 years.

If you have other threats in mind, feel free to leave a comment at the end of the post, and I’ll make sure to respond to you!

The Narrative

Professor Damodaran often reminds us that valuation is about narratives. There’s no such thing as a wrong narrative: my crystal ball is as good as yours and we’re all trying to forecast the unpredictable. The important thing is that you do have a story to tell and that your model fairly represents that.

Usually, I build my narrative to reflect the confidence I have in the company: the amount of years I dare to forecast solely depends on my understanding of the business and what I believe is the strength and durability of the competitive advantage. Wise is in the position to become a crucial player in a huge and key market. Therefore, I feel confident in explicitly forecasting 10 years.

As a McKinsey report explains (link), customer satisfaction will be a key factor of success in the cross-border payments industry. I would expand this concept to all industries, but consumer happiness is particularly pivotal when we’re talking about personal finances: people and businesses want safe, transparent, and cheap ways to handle their money, as wealth is often an essential part of everyone’s life. The banking sector has always been viewed with some skepticism (and frustration) due to the power asymmetry between customers and banks. Truth is before the 2010s there were few to no alternatives to traditional banks, but now people can choose, and customer satisfaction has become essential for market leadership.

The company’s outstanding focus on customers’ needs will keep bringing new users (and retain existing ones), and people will entrust more of their wealth to Wise, bringing total customer balances to £50 billion in 2034 from £13.3 billion in 2024.

Interest income on the first 1% gross yield will grow in line with customer balances. Instead, the portion attributed to interest above the 1% yield will reach 0 in 2028. Interest income is a function of rates set by central banks, and as I don’t want my valuation to be significantly skewed by macroeconomic views, I will just assume that rates will gradually decrease towards the 1% level, removing the impact of non-core operations from the valuation. I leave the option of higher rates for longer as an additional icing on the cake.

Wise will give back 46% (net of tax) of the interest earned on deposits through benefits paid to customers, in line with the cashback rates published by the company.

Finally, Wise will keep investing in its mission, lowering fees every 3 years by 5bps, reaching an average commission of 0,47% in 2034. Simultaneously, the company will grow its fee-related revenues to £6 billion, handling circa 5% of the market volume. Partnerships, especially in the baking sector, will contribute to capturing market share. Reputation is fundamental to building relationships with financial institutions, and as Wise establishes itself as a safe and efficient partner more companies will leverage its infrastructure. Specifically, Wise’s services are incredibly convenient for neo-banks, as demonstrated by the already existing partnerships with some of the biggest players in the sector, such as NuBank, N26, and Monzo. I believe this segment will bring consistent growth and reinforce Wise’s reputation, perhaps instituting a standard for the industry. Lastly, the fast-growing “card-only customer segment”, comprehending mostly travellers and people who use Wise as a satellite credit card, will contribute to the achievement of the £6 billion milestone, going from representing 17% of total customers in 2024 to 35% in 2034 (it was 4% in 2021).

In summary, Wise will emerge as a major player in the cross-border payments industry as its infrastructure integrates into the current value chain, enhancing efficiency and reducing costs. Partnerships with companies and institutions will drive growth, while the positive word-of-mouth effect will further reinforce the strong reputation amongst individuals. Finally, the entire market will benefit from regulatory tailwinds and increased transparency, further positioning Wise for success.

Valuation

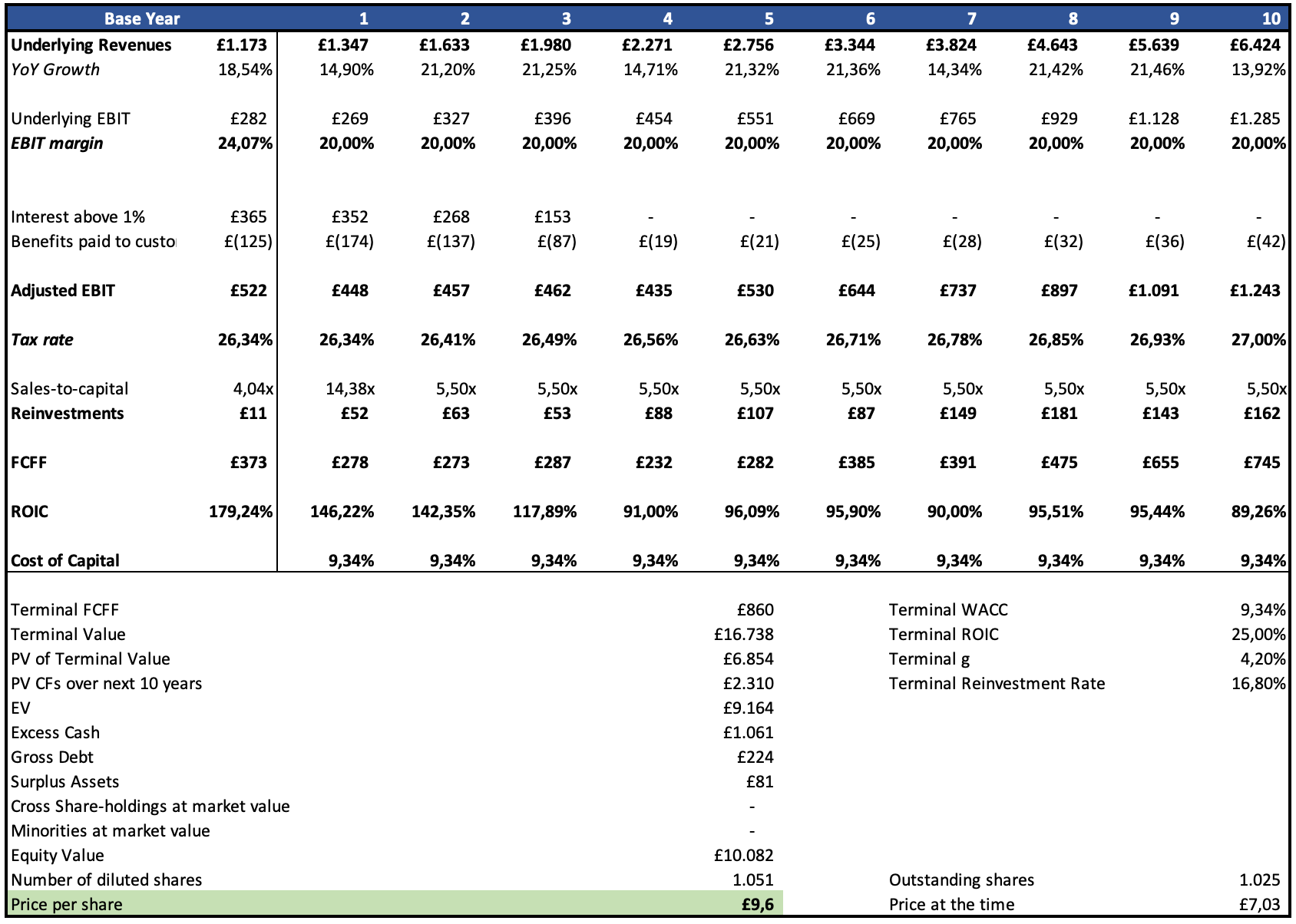

Modelling a narrative means attaching numbers to words. As mentioned, this model will include a 10-year explicit forecast before entering a stable growth phase.

First, underlying revenues, including fees and interest income on the first 1% yield, will grow at an 18.54% CAGR reaching £6.4 billion in 2034.

Second, as economies of scale kick in and Wise gradually cuts prices, margins will effectively stay fixed. Specifically, EBIT margin, adjusted for the capitalisation of technology and marketing expenses, will remain constant at 20%, a 4% decrease from the 2024 level.

As a result, bottom line EBIT, comprehending non-core operations, will grow at 9% CAGR to reach £1.2 billion in 2034.The tax rate will increase from 26.34% to 27%, as the company experiences increased benefits paid to consumers through cashbacks, which are taxed at 30% by authorities.

Wise’s business requires few investments to grow and function. Currently, the company boasts a 5.35x Invested Capital Turnover, meaning that for every dollar invested, the company receives $5.35 in additional revenues. As Wise’s reputation strengthens and both economies of scale and learning effects increase productivity, the company will be able to grow with little investments. Therefore, I set the Sales-to-capital ratio, a measure to estimate future reinvestment needs, to 5.5x. If you want to learn more about this ratio, check the first slides of this lecture by Damodaran: Sales-to-capital.

The FCFF will grow at a 9.15% CAGR and, excluding 2025 where margins decrease, the company averages a 49.72% marginal ROIC.

In 2034, Wise will enter the stable phase. Due to Wise’s competitive position and business model, I believe the company will maintain a ROIC > Cost of Capital. In particular, I set the terminal ROIC to 25% (the forecasted level in 2034 is 89%). In this case, growth does create value, and I fix the terminal g equal to the risk-free rate of 4.2%, the current yield on the 10Y GILT (as the valuation is carried out in pounds). The fundamental relationship between growth, ROIC, and reinvestment rate leads to the latter being 16.8% in the stable period.

Discounting back the cash flows, the target price for this Wise narrative is £9.6, representing a 37% upside from today’s £7.

Furthermore, even though I am not a great supporter of valuation multiples, I want to point out how Wise is cheap compared to its past. The company is currently trading at all-time-low multiples, strengthening the argument for a buying opportunity.

Finally, as competitors in the industry have significantly different business models (and many are private companies), performing a peer valuation makes little sense to me.

Conclusion

As usual, it is important to remember that I have no idea when the price will converge to value, but a few aspects point out that this could happen sooner rather than later.

First, Revolut is reportedly planning to undertake an IPO, seeking a $40 billion valuation which would result in 18.2 EV/Sales and 72.3 EV/EBIT, far greater than Wise’s 5.4 and 12 respective multiples. Revolut’s IPO could act as a catalyst as investors realise that the valuation gap between the two companies is too wide.

Second, individuals will more readily appreciate Wise’s value following the changes in reporting practices. The latest earnings release created some confusion, and markets hate confusion. Investors and professionals need to “translate” their views and adapt their models, and this often results in downward price pressure. Eventually, expectations will readjust, and Wise’s value will stand out.

Finally, the stock price encountered some support around the £6.8 level, which not only created a buying opportunity but also signalled a potential momentum shift.

Overall, the valuation looks particularly attractive given current market conditions, which saw July’s equity risk premium fall under the 4% level, as estimated by Damodaran.

Considering this investment’s risk-reward profile, where risk is defined as my confidence in the realisation of the narrative and reward as the potential upside, I allocated 18% of my portfolio to Wise at an av. entry price of £7.03, making it my second-biggest position.

If anyone reading this has a different narrative for Wise, I’ll be happy to discuss it and exchange perspectives to gain further insights!

Once again, thanks for taking the time to read this post. Have a great Summer and see you next time!

Hi Riccardo - great write-up!

Also sharing a recent Value Investor's Club write-up on WISE (if you haven't seen it already). It has a few more points to consider (especially in the comments section) - https://www.valueinvestorsclub.com/idea/WISE_PLC/2525212882

I'm also a Wise shareholder and I think it has a great future and follows Nick Sleep's "Scale Economics Shared" model.

One question on your DCF - what discount rate did you use?